- Pathwise estimation of covariate balancing propensity scores.

- Extract balancing weights from a balnet object.

- Extract coefficients from a balnet object.

- Extract coefficients from a cv.balnet object.

- Cross-validation for balnet.

- Plot diagnostics for a

balnetobject. - Plot diagnostics for a

cv.balnetobject. - Predict using a balnet object.

- Predict using a cv.balnet object.

- Print a balnet object.

- Print a cv.balnet object.

- Summarize a balnet object.

- Summarize a cv.balnet object.

-- B --

balnet()

balweights()

balweights.balnet()

balweights.cv.balnet()

-- C --

coef.balnet()

coef.cv.balnet()

cv.balnet()

-- P --

print.balweights.contrast()

print.coef.balnet.contrast()

plot.balnet()

plot.cv.balnet()

predict.balnet()

predict.cv.balnet()

print.balnet()

print.cv.balnet()

-- S --

summary.balweights.contrast()

summary.coef.balnet.contrast()

summary.balnet()

summary.cv.balnet()

Pathwise estimation of covariate balancing propensity scores.

Description

Fits regularized logistic regression models using covariate balancing loss functions, yielding balancing weights targeting the ATE, ATT, or treated/control means.

Usage

balnet(

X,

W,

target = c("ATE", "ATT", "treated", "control"),

sample.weights = NULL,

max.imbalance = NULL,

nlambda = 100L,

lambda.min.ratio = 0.01,

lambda = NULL,

penalty.factor = NULL,

groups = NULL,

alpha = 1,

standardize = TRUE,

tol = 1e-07,

maxit = as.integer(1e+05),

verbose = FALSE,

num.threads = 1L,

...

)Arguments

X |

A numeric matrix or data frame with pre-treatment covariates. |

W |

Treatment vector (0 = control, 1 = treated). |

target |

The target estimand. Default is "ATE". |

sample.weights |

Optional sample weights. If |

max.imbalance |

Optional upper bound on the standardized covariate imbalance. For lasso penalization

( |

nlambda |

Number of values for |

lambda.min.ratio |

Ratio of smallest to largest lambda. Default is 1e-2. |

lambda |

Optional |

penalty.factor |

Penalty factor per feature. Default is 1 (i.e., each feature receives the same penalty). If groups are specified, the penalty factors default to the square root of each group size. |

groups |

Optional list of group indices for group penalization. |

alpha |

Elastic net mixing parameter. Default is 1 (lasso), 0 corresponds to ridge.

For |

standardize |

Whether to standardize the input matrix. Should only be |

tol |

Coordinate descent convergence tolerance. Default is 1e-7. |

maxit |

Maximum number of coordinate descent iterations. Default is 1e5. |

verbose |

Whether to display information during fitting. Default is |

num.threads |

Number of threads to use. Default is 1. |

... |

Additional internal arguments passed to the solver. |

Details

This function aims to find balancing weights \(\hat\gamma_i\), using logistic propensity scores, that balance covariate means to a target vector, i.e.,

$$\frac{1}{n} \sum_{i=1}^n \hat\gamma_i X_i = \bar X_{\mathrm{target}}.$$

With lasso regularization (alpha = 1), imbalance is controlled in the \(\ell_\infty\) sense,

allowing absolute slack of at most \(\lambda\) per covariate.

For target = "ATE", two logistic models are fit, one per arm, with

$$\hat\gamma_i^{(1)} = \frac{W_i}{\hat e^{(1)}(X_i)}, \quad \hat\gamma_i^{(0)} = \frac{1 - W_i}{1 - \hat e^{(0)}(X_i)}, \quad \bar X_{\mathrm{target}} = \frac{1}{n} \sum_{i=1}^n X_i.$$

\(\hat e^{(w)}(X_i)\) is the fitted propensity score for arm \(w\).

For target = "ATT", weights balance the control means:

$$\hat\gamma_i = (1 - W_i) \frac{\hat e^{(0)}(X_i)}{1 - \hat e^{(0)}(X_i)}, \quad \bar X_{\mathrm{target}} = \frac{1}{\sum W_i} \sum_{i=1}^n W_i X_i.$$

Value

A fit balnet object.

References

Sverdrup, Erik and Trevor Hastie. "balnet: Pathwise Estimation of Covariate Balancing Propensity Scores". arXiv preprint, arXiv:2602.18577, 2026.

Examples

# Simulate data with confounding.

n <- 2000

p <- 10

X <- matrix(rnorm(n * p), n, p)

W <- rbinom(n, 1, 1 / (1.5 + exp(X[, 2] + X[, 3])))

Y <- W + 2 * log(1 + exp(X[, 1] + X[, 2] + X[, 3])) + rnorm(n)

# Fit model targeting the ATE = E[Y(1)] - E[Y(0)].

# Two logistic models are fit: one for treated, one for control.

fit <- balnet(X, W, target = "ATE")

# Print path summary.

print(fit)

#> Call: balnet(X = X, W = W, target = "ATE")

#>

#> Control (path: 100/100)

#> Nonzero Avg|SMD| Lambda

#> 1 0 0.049101 0.192893

#> 2 1 0.048360 0.184125

#> 3 2 0.046846 0.175756

#> ...

#> 98 10 0.002117 0.002117

#> 99 10 0.002021 0.002021

#> 100 10 0.001929 0.001929

#>

#> Treated (path: 100/100)

#> Nonzero Avg|SMD| Lambda

#> 1 0 0.080111 0.314719

#> 2 2 0.078623 0.300415

#> 3 2 0.076021 0.286761

#> ...

#> 98 10 0.003454 0.003454

#> 99 10 0.003297 0.003297

#> 100 10 0.003147 0.003147

# Visualize the path.

plot(fit)

plot(fit, lambda = 0)

# Predict propensity scores at end of lambda path.

W.hat <- predict(fit, X, lambda = 0)

# Get balancing weights at end of lambda path.

ipw.weights <- balweights(fit, lambda = 0)

# Estimate ATE using balancing weights.

mean(Y * (ipw.weights$treated - ipw.weights$control))

#> [1] 0.8594794

Extract balancing weights from a balnet object.

Description

Convenience method for extracting the estimated balancing weights \(\hat{\gamma}\). Under unconfoundedness, these correspond to inverse probability weights (IPW) for standard treatment effect estimands and are computed from the fitted covariate balancing propensity scores.

Usage

balweights(object, lambda = NULL, ...)

## S3 method for class 'balnet'

balweights(object, lambda = NULL, ...)

## S3 method for class 'balweights.contrast'

print(x, ...)

## S3 method for class 'balweights.contrast'

summary(object, ...)

## S3 method for class 'cv.balnet'

balweights(object, lambda = "lambda.min", ...)Arguments

object |

A |

lambda |

Value(s) of the penalty parameter

|

... |

Additional arguments (currently ignored). |

x |

A |

Value

Estimated balancing weights (for dual-arm fits, returns a list with entries for each arm).

Examples

n <- 100

p <- 25

X <- matrix(rnorm(n * p), n, p)

W <- rbinom(n, 1, 1 / (1 + exp(1 - X[, 1])))

# Fit an ATT model.

fit <- balnet(X, W, target = "ATT")

# Extract balancing weights over fit lambda sequence.

wts <- balweights(fit)

# Extract balancing weights at specified lambda.

wts <- balweights(fit, lambda = 0)

Extract coefficients from a balnet object.

Description

Extract coefficients from a balnet object.

Usage

## S3 method for class 'balnet'

coef(object, lambda = NULL, ...)

## S3 method for class 'coef.balnet.contrast'

print(x, ...)

## S3 method for class 'coef.balnet.contrast'

summary(object, ...)Arguments

object |

A |

lambda |

Value(s) of the penalty parameter

|

... |

Additional arguments (currently ignored). |

x |

A |

Value

Estimated logistic coefficients (for dual-arm fits, returns a list with entries for each arm).

Examples

n <- 100

p <- 25

X <- matrix(rnorm(n * p), n, p)

W <- rbinom(n, 1, 1 / (1 + exp(1 - X[, 1])))

# Fit an ATT model.

fit <- balnet(X, W, target = "ATT")

# Extract coefficients over fit lambda sequence.

coefs <- coef(fit)

# Extract coefficients at specified lambda.

coefs <- coef(fit, lambda = 0)

Extract coefficients from a cv.balnet object.

Description

Extract coefficients from a cv.balnet object.

Usage

## S3 method for class 'cv.balnet'

coef(object, lambda = "lambda.min", ...)Arguments

object |

A |

lambda |

The lambda to use. Defaults to the cross-validated lambda. |

... |

Additional arguments (currently ignored). |

Value

Estimated logistic coefficients (for dual-arm fits, returns a list with entries for each arm).

Examples

n <- 100

p <- 25

X <- matrix(rnorm(n * p), n, p)

W <- rbinom(n, 1, 1 / (1 + exp(1 - X[, 1])))

# Fit an ATT model.

cv.fit <- cv.balnet(X, W, target = "ATT")

# Extract coefficients at cross-validated lambda.

coefs <- coef(cv.fit)

Cross-validation for balnet.

Description

Cross-validation for balnet.

Usage

cv.balnet(

X,

W,

type.measure = c("balance.loss"),

nfolds = 10,

foldid = NULL,

...

)Arguments

X |

A numeric matrix or data frame with pre-treatment covariates. |

W |

Treatment vector (0: control, 1: treated). |

type.measure |

The loss to minimize for cross-validation. Default is balance loss. |

nfolds |

The number of folds used for cross-validation, default is 10. |

foldid |

An optional |

... |

Arguments for |

Value

A fit cv.balnet object.

Examples

n <- 100

p <- 25

X <- matrix(rnorm(n * p), n, p)

W <- rbinom(n, 1, 1 / (1 + exp(1 - X[, 1])))

# Fit an ATE model.

cv.fit <- cv.balnet(X, W)

# Print CV summary.

print(cv.fit)

#> Call: cv.balnet(X = X, W = W)

#>

#> Cross-validated lambda minimizing type.measure = balance.loss:

#> Arm Nonzero Avg|SMD| Lambda Index

#> Control 8 0.04365 0.06699 17

#> Treated 3 0.12185 0.27357 6

# Plot at cross-validated lambda.

plot(cv.fit)

# Predict at cross-validated lambda.

W.hat <- predict(cv.fit, X)

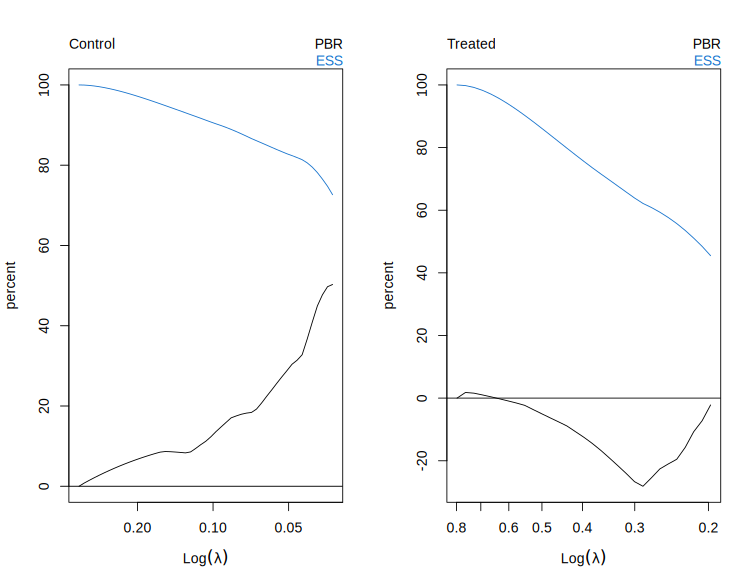

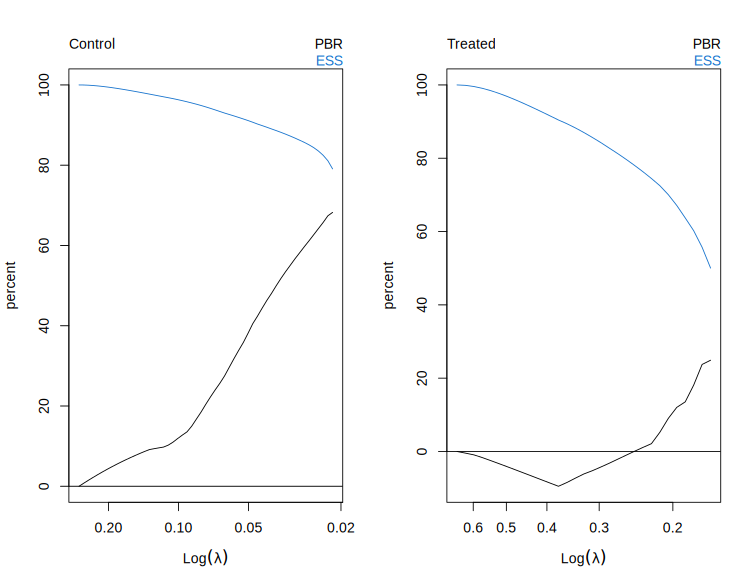

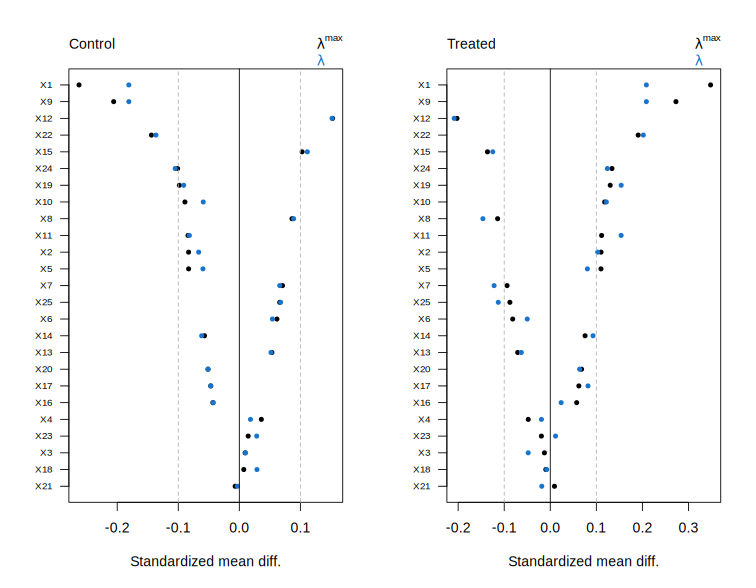

Plot diagnostics for a balnet object.

Description

Shows effective sample size (ESS) and percent bias reduction (PBR; reduction

in mean absolute imbalance) along the regularization path, computed from balancing

weights and normalized to percentages. The right-hand axis maps these values

to the coefficient of variation (CV) of the weights.

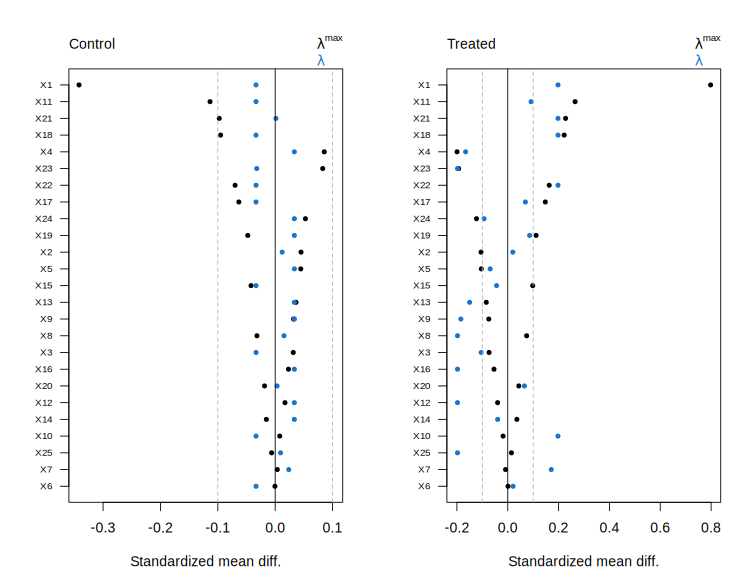

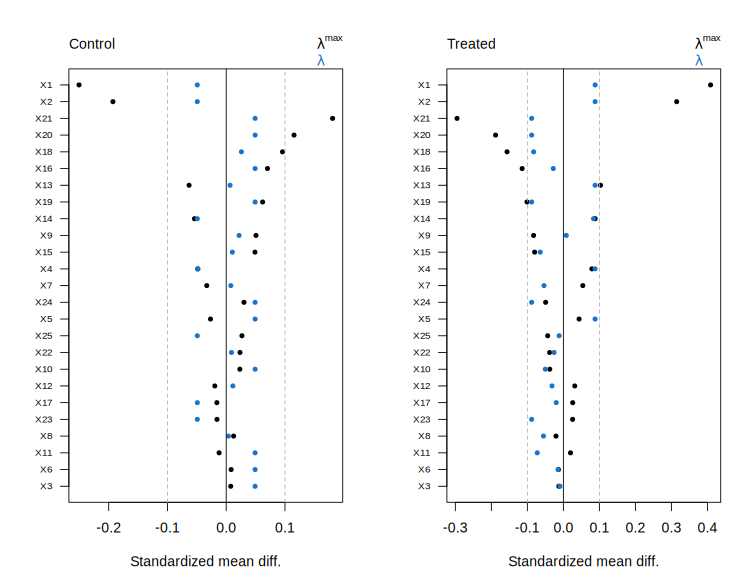

Supplying the lambda argument displays the standardized covariate imbalance

\((\bar X_{\mathrm{weighted}} - \bar X_{\mathrm{target}}) / \sigma_{\mathrm{target}}\),

computed using the balancing weights at the specified lambda.

Usage

## S3 method for class 'balnet'

plot(x, lambda = NULL, groups = NULL, max = NULL, ...)Arguments

x |

A |

lambda |

If NULL (default) diagnostics over the lambda path is shown. Otherwise, covariate balance at provided lambda value is shown (if target = "ATE", lambda can be a 2-vector, arm 0 and arm 1.) |

groups |

Optional named list of contiguous covariate index ranges to

aggregate into a single variable before computing covariate imbalance

(e.g., |

max |

The number of covariates to display in covariate balance plot. Defaults to all covariates. |

... |

Additional arguments. |

Value

Invisibly returns the information underlying the plot.

Examples

n <- 100

p <- 25

X <- matrix(rnorm(n * p), n, p)

W <- rbinom(n, 1, 1 / (1 + exp(1 - X[, 1])))

# Fit an ATT model.

fit <- balnet(X, W, target = "ATT")

# Plot the five covariates with the largest unweighted imbalance

plot(fit, lambda = 0, max = 5)

Plot diagnostics for a cv.balnet object.

Description

Plot diagnostics for a cv.balnet object.

Usage

## S3 method for class 'cv.balnet'

plot(x, lambda = "lambda.min", ...)Arguments

x |

A |

lambda |

The lambda to use. Defaults to the cross-validated lambda. |

... |

Additional arguments. |

Value

Invisibly returns the information underlying the plot.

Examples

n <- 100

p <- 25

X <- matrix(rnorm(n * p), n, p)

W <- rbinom(n, 1, 1 / (1 + exp(1 - X[, 1])))

# Fit an ATT model.

cv.fit <- cv.balnet(X, W, target = "ATT")

# Plot at cross-validated lambda.

plot(cv.fit)

Predict using a balnet object.

Description

Predict using a balnet object.

Usage

## S3 method for class 'balnet'

predict(object, newdata, lambda = NULL, type = c("response", "link"), ...)Arguments

object |

A |

newdata |

A numeric matrix. |

lambda |

Value(s) of the penalty parameter

|

type |

The type of predictions. Default is "response" (propensity scores). |

... |

Additional arguments (currently ignored). |

Value

Estimated predictions (for dual-arm fits, returns a list with entries for each arm).

Examples

n <- 100

p <- 25

X <- matrix(rnorm(n * p), n, p)

W <- rbinom(n, 1, 1 / (1 + exp(1 - X[, 1])))

# Fit an ATT model.

fit <- balnet(X, W, target = "ATT")

# Predict propensity scores over fit lambda sequence.

W.hat <- predict(fit, X)

Predict using a cv.balnet object.

Description

Predict using a cv.balnet object.

Usage

## S3 method for class 'cv.balnet'

predict(object, newdata, lambda = "lambda.min", type = c("response"), ...)Arguments

object |

A |

newdata |

A numeric matrix. |

lambda |

The lambda to use. Defaults to the cross-validated lambda. |

type |

The type of predictions. Default is "response" (propensity scores). |

... |

Additional arguments (currently ignored). |

Value

Estimated predictions (for dual-arm fits, returns a list with entries for each arm).

Examples

n <- 100

p <- 25

X <- matrix(rnorm(n * p), n, p)

W <- rbinom(n, 1, 1 / (1 + exp(1 - X[, 1])))

# Fit an ATT model.

cv.fit <- cv.balnet(X, W, target = "ATT")

# Predict propensity scores at cross-validated lambda.

W.hat <- predict(cv.fit, X)

Print a balnet object.

Description

Print a balnet object.

Usage

## S3 method for class 'balnet'

print(x, digits = max(3L, getOption("digits") - 3L), max = 3, ...)Arguments

x |

A |

digits |

Number of digits to print. |

max |

Total number of rows to show from the beginning and end of the path |

... |

Additional print arguments. |

Value

Invisibly returns the printed information.

Examples

n <- 100

p <- 25

X <- matrix(rnorm(n * p), n, p)

W <- rbinom(n, 1, 1 / (1 + exp(1 - X[, 1])))

# Fit an ATT model.

fit <- balnet(X, W, target = "ATT")

# Print path summary.

print(fit)

#> Call: balnet(X = X, W = W, target = "ATT")

#>

#> Control (path: 51/100)

#> Nonzero Avg|SMD| Lambda

#> 1 0 0.19807 0.73400

#> 2 1 0.19670 0.70064

#> 3 1 0.19557 0.66879

#> ...

#> 49 19 0.06944 0.07870

#> 50 20 0.06963 0.07513

#> 51 22 0.06676 0.07171

Print a cv.balnet object.

Description

Print a cv.balnet object.

Usage

## S3 method for class 'cv.balnet'

print(x, digits = max(3L, getOption("digits") - 3L), ...)Arguments

x |

A |

digits |

Number of digits to print. |

... |

Additional print arguments. |

Value

Invisibly returns the printed information.

Examples

n <- 100

p <- 25

X <- matrix(rnorm(n * p), n, p)

W <- rbinom(n, 1, 1 / (1 + exp(1 - X[, 1])))

# Fit an ATT model.

cv.fit <- cv.balnet(X, W, target = "ATT")

# Print CV summary.

print(cv.fit)

#> Call: cv.balnet(X = X, W = W, target = "ATT")

#>

#> Cross-validated lambda minimizing type.measure = balance.loss:

#> Arm Nonzero Avg|SMD| Lambda Index

#> Control 1 0.2531 0.9778 4

Summarize a balnet object.

Description

Summarize a balnet object.

Usage

## S3 method for class 'balnet'

summary(object, ...)Arguments

object |

|

... |

Additional summary arguments. |

Value

Returns the printed information.

Summarize a cv.balnet object.

Description

Summarize a cv.balnet object.

Usage

## S3 method for class 'cv.balnet'

summary(object, ...)Arguments

object |

|

... |

Additional summary arguments. |

Value

Returns the printed information.